Tenneco Reports First Quarter 2016 Results

- Record-high 1Q revenue, outpacing industry production

- Record-high EBIT, net income and EPS

- Operating cash performance improves 42% year-over-year

- Raising full-year revenue outlook

Lake Forest, Illinois, April 26, 2016 – Tenneco (NYSE: TEN) reported first quarter net income of $57 million, or 99-cents per diluted share, compared with $49 million, or 80-cents per diluted share in first quarter 2015. Adjusted net income rose 24% to a first quarter record high of $67 million, or $1.17 per diluted share, versus $54 million or 88-cents per diluted share last year, a 33% improvement in adjusted earnings per share.

Revenue

Total revenue in the first quarter was $2.136 billion, up 6% year-over-year. Excluding a negative currency impact of $69 million, total first quarter revenue increased 9% to $2.205 billion. Tenneco’s total revenue excluding currency significantly outgrew global aggregate industry production growth of 1% in the quarter driven by light vehicle revenue growth of 11%, led by North America, Europe, China and India; commercial truck and off-highway revenue growth of 1%; and an 8% increase in global aftermarket revenue on higher sales in Europe, South America and North America.

“We are off to a strong start for the year with outstanding first quarter results including strong revenue growth, record-high earnings, and our twelfth consecutive quarter of margin improvement,” said Gregg Sherrill, chairman and CEO, Tenneco. “In addition to delivering on our growth plans, we drove higher earnings and improved margins with a disciplined approach to improving manufacturing efficiency and lowering our cost structure. This consistent quarterly performance demonstrates solid execution on our strategies for achieving profitable growth while continuing to plan and invest for the future.”

EBIT

First quarter EBIT (earnings before interest, taxes and noncontrolling interests) increased to $124 million, versus $120 million last year. Adjusted EBIT rose 10% to $138 million, a record high for the first quarter. Adjusted EBIT includes $12 million in negative currency. The record-high first quarter EBIT was driven by strong light vehicle volumes, commercial truck and off-highway clean air content growth, higher global aftermarket sales and operational cost improvements.

Adjusted first quarter 2016 and 2015 results

| Q1 2016 | Q1 2015 | |||||||||||||||||

| (millions except per share amounts) | EBITDA* | EBIT | Net income attributable to Tenneco Inc. | Per Share | EBITDA* | EBIT | Net income attributable to Tenneco Inc. | Per Share | ||||||||||

| Earnings Measures | $ | 178 | $ | 124 | $ | 57 | $ | 0.99 | $ | 170 | $ | 120 | $ | 49 | $ | 0.80 | ||

| Adjustments (reflects non-GAAP measures): | ||||||||||||||||||

| Restructuring and related expenses | 11 | 14 | 13 | 0.23 | 5 | 5 | 4 | 0.07 | ||||||||||

| Net tax adjustments | - | - | (3) | (0.05) | - | - | 1 | 0.01 | ||||||||||

| Non-GAAP earnings measures | $ | 189 | $ | 138 | $ | 67 | $ | 1.17 | $ | 175 | $ | 125 | $ | 54 | $ | 0.88 | ||

First quarter EBIT margin

In the first quarter 2016, Tenneco delivered its twelfth consecutive quarter of value-add adjusted EBIT margin improvement with higher margins in both product lines.

|

|

Q1 2016 | Q1 2015 | ||

| EBIT as a percent of revenue | 5.8% | 5.9% | ||

| EBIT as a percent of value-add revenue | 7.6% | 7.7% | ||

| Adjusted EBIT as a percent of revenue | 6.5% | 6.2% | ||

| Adjusted EBIT as a percent of value-add revenue | 8.5% | 8.0% | ||

Clean Air adjusted EBIT as a percent of value-add revenue was up 110 basis points to 11%, driven by higher light vehicle volumes and new platform launches, as well as commercial truck and off-highway content growth and higher aftermarket revenue in North America. Ride Performance adjusted EBIT margin improved 100 basis points to 10.1%, driven by stronger light vehicle volumes in Europe, India and China and higher aftermarket sales in Europe, South America and North America. Both Clean Air and Ride Performance margins include the benefit of operational cost improvements.

Cash

Cash used by operations in the quarter was $29 million, a 42% improvement compared with a cash use of $50 million a year ago. The improvement was driven by higher earnings and strong working capital management.

During the quarter the company repurchased 360,000 shares of common stock for $16 million. Since January 1, 2015, the company has repurchased a total of 4.6 million shares of common stock for $229 million.

OUTLOOK

Second quarter 2016

Tenneco expects total revenue growth of 6% in the second quarter 2016 (excluding currency), outpacing estimated aggregate industry production growth of 4% which includes an increase in light vehicle industry production of 4% and a 1% decline in combined commercial truck and off-highway industry production.

Based on current exchange rates, the company anticipates no significant currency headwinds in the second quarter.

Tenneco’s expected 6% revenue increase will be driven by stronger global light vehicle volumes including new launches and the ramp up on recently launched platforms, and a solid contribution from the global aftermarket. Commercial truck and off-highway revenue is expected to be roughly in line with industry production.

The company also expects continued margin improvement in the second quarter.

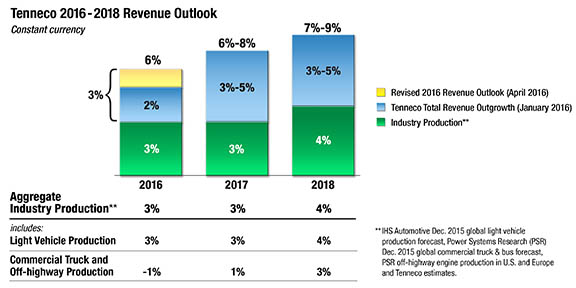

Revised Full Year Revenue Outlook

Tenneco is upwardly revising its revenue guidance for the full year. The company now expects to outgrow global industry production by 3 percentage points, resulting in annual revenue growth of 6 percent, excluding currency based on current aggregate industry production estimates.

“Given our first quarter results and based on what we see in the markets today, we expect to deliver full year revenue growth that exceeds industry production by 3%. Looking beyond this year, we see our growth accelerating in both 2017 and 2018 primarily due to new light vehicle emissions regulations beginning to take effect in North America and Europe,” said Sherrill. “We also expect continued margin improvement as we leverage higher volumes and execute on our operational improvement initiatives.”

*Aggregate Industry Production: IHS Automotive April 2016 global light vehicle production forecasts, Power Systems Research (PSR), April 2016 forecast for global commercial truck and buses and PSR off-highway engine production in North America and Europe and Tenneco estimates.

Click here to download Q1 2016 release including all attachments listed below

Attachment 1

Statements of Income – 3 Months

Balance Sheets

Statements of Cash Flows – 3 Months

Attachment 2

Reconciliation of GAAP Net Income to EBITDA including noncontrolling interests – 3 Months

Reconciliation of GAAP to Non-GAAP Earnings Measures – 3 Months

Reconciliation of GAAP Revenue to Non-GAAP Revenue Measures – 3 Months

Reconciliation of GAAP Revenue to Non-GAAP Revenue Measures – 3 Months

Reconciliation of Non-GAAP Measures – Debt Net of Cash/Adjusted LTM EBITDA including noncontrolling interests

Reconciliation of GAAP Revenue to Non-GAAP Revenue Measures – Original Equipment and Aftermarket Revenue – 3 Months

Reconciliation of GAAP Revenue and Earnings to Non-GAAP Revenue and Earnings Measures – 3 Months

Reconciliation of GAAP Revenue to Non-GAAP Revenue Measures – Original Equipment Commercial Truck, Off-Highway and other revenues – 3 Months

CONFERENCE CALL

The company will host a conference call on Tuesday, April 26, 2016 at 9:00 a.m. ET. The dial-in number is 800-988-9663 (domestic) or 517-308-9192 (international). The passcode is TENNECO. The call and accompanying slides will be available on the financial section of the Tenneco web site at www.tenneco.com. A recording of the call will be available one hour following completion of the call on April 26, 2016 through May 26, 2016. To access this recording, dial 866-481-4961 (domestic) or 203-369-1557 (international). The purpose of the call is to discuss the company’s operations for the first fiscal quarter of 2016, as well as provide updated information regarding matters impacting the company’s outlook. A copy of the press release is available on the financial and news sections of the Tenneco web site.

ANNUAL MEETING

The Tenneco Board of Directors has scheduled the corporation’s annual meeting of shareholders for Wednesday, May 18, 2016 at 10:00 a.m. CT. The meeting will be held at the corporate headquarters, 500 North Field Drive, Lake Forest, Illinois.

Tenneco is an $8.2 billion global manufacturing company with headquarters in Lake Forest, Illinois and approximately 30,000 employees worldwide. Tenneco is one of the world’s largest designers, manufacturers and marketers of clean air and ride performance products and systems for automotive and commercial vehicle original equipment markets and the aftermarket. Tenneco’s principal brand names are Monroe®, Walker®, XNOx™ and Clevite®Elastomers.

Revenue estimates in this release are based on OE manufacturers’ programs that have been formally awarded to the company; programs where Tenneco is highly confident that it will be awarded business based on informal customer indications consistent with past practices; and Tenneco’s status as supplier for the existing program and its relationship with the customer. These revenue estimates are also based on anticipated vehicle production levels and pricing, including precious metals pricing and the impact of material cost changes. For certain additional assumptions upon which these estimates are based, see the slides accompanying the April 26, 2016 webcast, which will be available on the financial section of the Tenneco website at www.tenneco.com.

This press release contains forward-looking statements. Words such as “may,” “expects,” “anticipate,” ”projects,” “will,” “outlook” and similar expressions identify forward-looking statements. These forward-looking statements are based on the current expectations of the company (including its subsidiaries). Because these forward-looking statements involve risks and uncertainties, the company's plans, actions and actual results could differ materially. Among the factors that could cause these plans, actions and results to differ materially from current expectations are:

(i) general economic, business and market conditions;

(ii) the company’s ability to source and procure needed materials, components and other products and services in accordance with customer demand and at competitive prices;

(iii) the cost and outcome of existing and any future claims, legal proceedings, or investigations, including, but not limited to, any of the foregoing arising in connection with the ongoing global antitrust investigation, product performance, product safety or intellectual property rights;

(iv) changes in capital availability or costs, including increases in the company's costs of borrowing (i.e., interest rate increases), the amount of the company's debt, the ability of the company to access capital markets at favorable rates, and the credit ratings of the company’s debt;

(v) changes in consumer demand, prices and the company’s ability to have our products included on top selling vehicles, including any shifts in consumer preferences to lower margin vehicles, for which we may or may not have supply arrangements;

(vi) changes in automotive and commercial vehicle manufacturers' production rates and their actual and forecasted requirements for the company's products such as the significant production cuts during recent years by automotive manufacturers in response to difficult economic conditions;

(vii) the overall highly competitive nature of the automobile and commercial vehicle parts industries, and any resultant inability to realize the sales represented by the company’s awarded book of business which is based on anticipated pricing and volumes over the life of the applicable program;

(viii) the loss of any of our large original equipment manufacturer (“OEM”) customers (on whom we depend for a substantial portion of our revenues), or the loss of market shares by these customers if we are unable to achieve increased sales to other OEMs or any change in customer demand due to delays in the adoption or enforcement of worldwide emissions regulations;

(ix) the company's continued success in cost reduction and cash management programs and its ability to execute restructuring and other cost reduction plans, including our current European cost reduction initiatives, and to realize anticipated benefits from these plans;

(x) economic, exchange rate and political conditions in the countries where we operate or sell our products;

(xi) workforce factors such as strikes or labor interruptions;

(xii) increases in the costs of raw materials, including the company’s ability to successfully reduce the impact of any such cost increases through materials substitutions, cost reduction initiatives, customer recovery and other methods;

(xiii) the negative impact of fuel price volatility on transportation and logistics costs, raw material costs, discretionary purchases of vehicles or aftermarket products, and demand for off-highway equipment;

(xiv) the cyclical nature of the global vehicular industry, including the performance of the global aftermarket sector and longer product lives of automobile parts;

(xv) product warranty costs;

(xvi) the failure or breach of our information technology systems and the consequences that such failure or breach may have to our business;

(xvii) the company's ability to develop and profitably commercialize new products and technologies, and the acceptance of such new products and technologies by the company's customers and the market;

(xviii) changes by the Financial Accounting Standards Board or other accounting regulatory bodies to authoritative generally accepted accounting principles or policies;

(xix) changes in accounting estimates and assumptions, including changes based on additional information;

(xx) the impact of the extensive, increasing and changing laws and regulations to which we are subject, including environmental laws and regulations, which may result in our incurrence of environmental liabilities in excess of the amount reserved;

(xxi) natural disasters, acts of war and/or terrorism and the impact of these occurrences or acts on economic, financial, industrial and social condition, including, without limitation, with respect to supply chains and customer demand in the countries where the company operates; and

(xxii) the timing and occurrence (or non-occurrence) of transactions and events which may be subject to circumstances beyond the control of the company and its subsidiaries.

The company undertakes no obligation to update any forward-looking statement to reflect events or circumstances after the date of this press release. Additional information regarding these risk factors and uncertainties is detailed from time to time in the company's SEC filings, including but not limited to its annual report on Form 10-K for the year ended December 31, 2015.

###

Investor inquiries:

Linae Golla

847-482-5162

lgolla@tenneco.com

Media inquiries:

Bill Dawson

847-482-5807

bdawson@tenneco.com